Two years after our2024 golf taxation analysis, we return to Southeast Asia’s golf markets with updated data from industry experts across seven countries. What we found reveals not gradual convergence toward regional standards, but a widening competitive chasm with tax policy increasingly determining which markets thrive and which struggle despite superior natural assets.

The central question is no longer “whether” golf taxation matters to competitiveness. The data conclusively answers yes. The real question is: can world-class course design and destination appeal overcome a 15–20 percentage point tax disadvantage? Vietnam is the test case, and the results are … complicated.

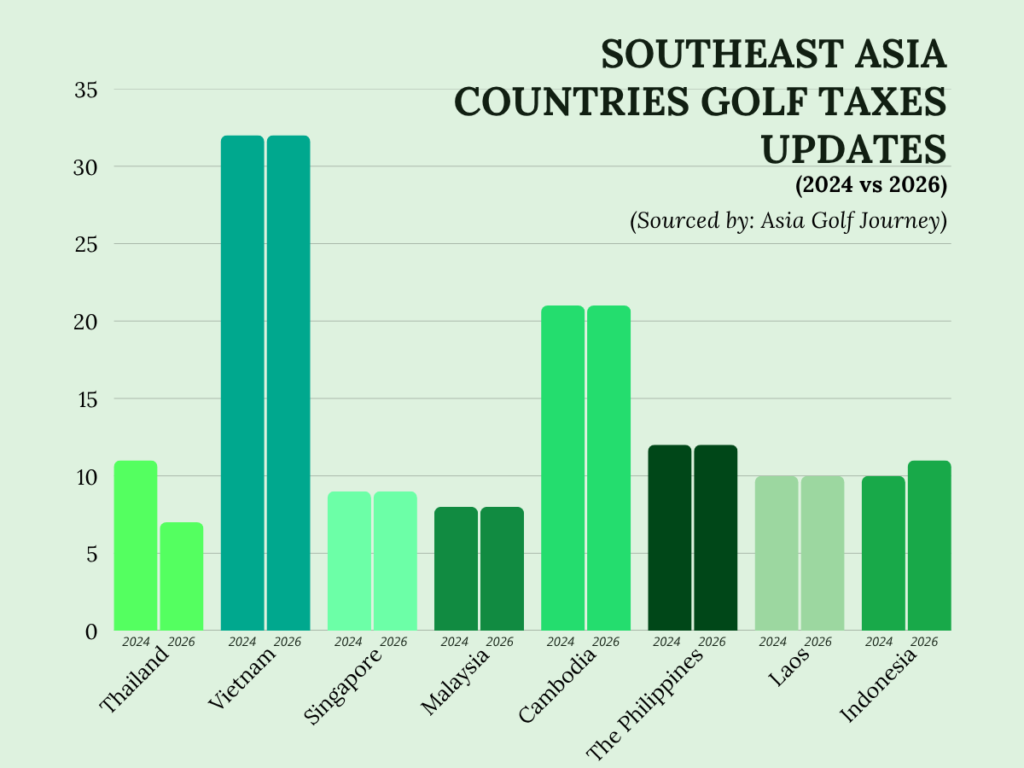

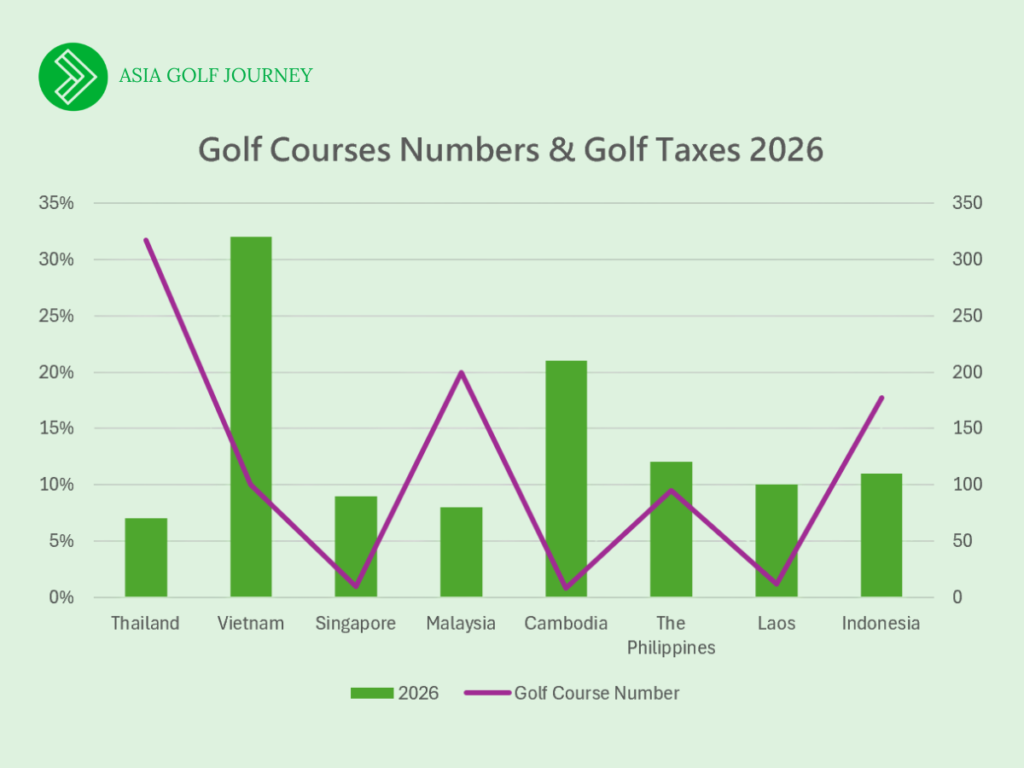

Southeast Asia’s golf markets operate under dramatically different tax regimes, creating competitive advantages and disadvantages that no amount of superior greenkeeping can fully offset. Our 2026 analysis reveals total tax burdens ranging from 7% in Thailand to 32% in Vietnam, a spread that translates to $30–$50 in price differences on a typical $150 round.

The government’s decision to extend the reduced 7% VAT through 2026 (down from the standard 10%) gives golf operators a 3-percentage-point structural advantage over the regional baseline.

Mr. Simon Mees, General Manager at Absolute Golf Solution Thailand, describes the impact:

“The standard VAT rate is 10%, but the government reduced this to 7% extended through 2026. This tax relief is significant, but success requires more than favorable rates. The Thai golf market remains strong but increasingly competitive. Demand is strong, supported by tourism growth, but operators face margin pressure from rising costs and regional competition. Success is now driven more by yield management, market mix, and integrated resort offerings rather than volume alone, along with strong demand from the local market, which again is competitive given the high number of quality golf courses and resorts in the country.”

Thailand’s challenge isn’t tax policy it’s maintaining differentiation as Vietnam closes quality gaps. Mees notes a critical shift:

“There is a clear shift toward higher-value international golfers, particularly from long-haul markets, while some short-haul demand has softened. Domestic golfers remain important but are generally more price-sensitive and promotion-driven. Overall, focus has moved from volume to quality of spend per visitor. AGS have developed strong commercial strategies to drive performance at our managed clubs and resorts.”

This “high-value tourism” pivot is evident across Thailand’s golf sector. The government launched the “Amazing 5 Economy” initiative (2025–2026), targeting experiential travelers willing to pay premiums for unique experiences. Golf fits perfectly: courses like Siam Country Club, Black Mountain, Blue Canyon, and Laguna Phuket attract golfers spending $200–$300 per round, plus resort accommodation, F&B, and activities.

But here is Thailand’s deeper strategic insight: tax relief alone isn’t enough. As Mees emphasizes:

“Success will depend on differentiation through service quality, course conditioning, brand positioning, and total destination experience, rather than simply focused on increasing round volumes. Thailand’s established reputation remains a key strength, but continued business innovation and strategic investment and development of facilities along with developing people, that will enable them to perform to a higher level.”

Tax advantages create opportunity. Execution determines results. Thailand leverages its 7% rate not for price competition, but to invest margins in superior conditioning, professional staff development, and integrated resort experiences that justify premium positioning.

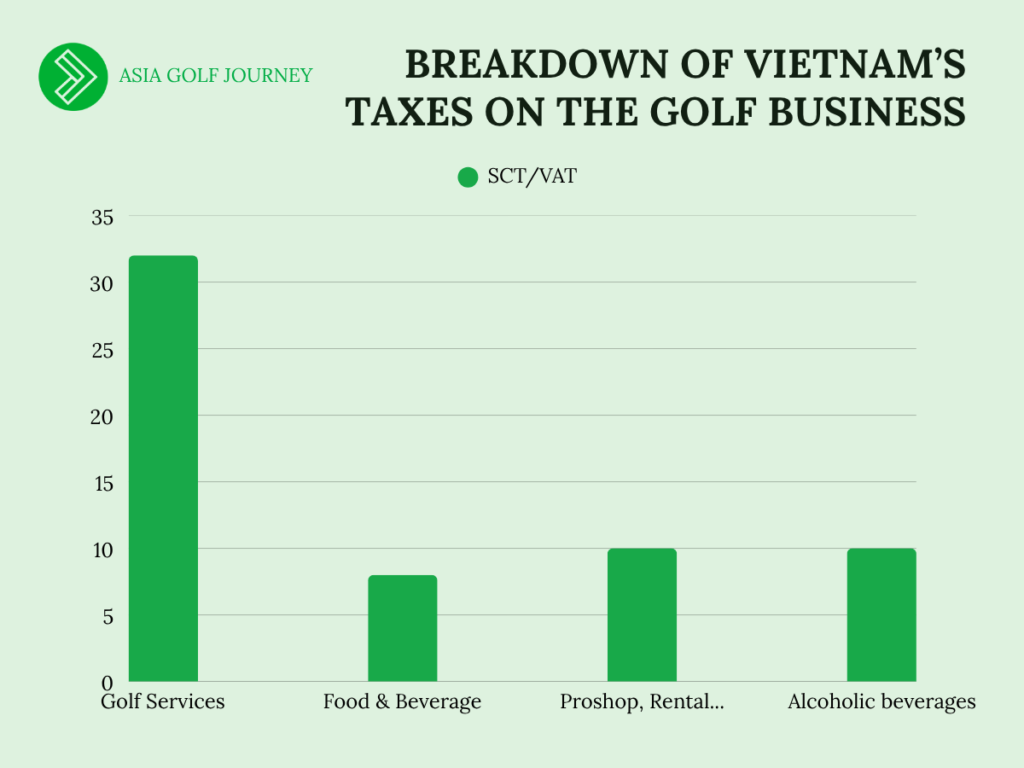

Vietnam presents Southeast Asia’s sharpest contradiction: the region’s fastest-growing golf market operates under its most punitive tax structure. The country welcomed a historic record of nearly 21.2 million international tourists in 2025, a 20.4% increase over 2024, exceeding pre-pandemic levels by 17.8% with golf tourism revenue reaching an estimated $1 billion. Yet every round played carries a 32% combined VAT and Special Consumption Tax, classifying golf alongside gambling and luxury cars.

Ms. Hien Ton, Director of Sales at Laguna Golf Lang Co, Hue, frames the paradox:

“Total taxes on golf services: 10% VAT plus 20% luxury tax, create a significant price barrier. But here’s what’s interesting: has demand from international golfers changed in the past 12 months? Yes. We’re seeing increased inbound activity with longer-stay golfers drawn by generously reasonable prices in central Vietnam.”

“Reasonable prices” with a 32% tax rate? The explanation lies in Vietnam’s broader value equation: while golf is taxed heavily, accommodation, dining, transport, and activities remain highly affordable. A golfer paying $150 for a round (inclusive of taxes) might stay at a beachfront hotel for $80 per night and enjoy $15 gourmet dinners. The total trip cost still undercuts many competing destinations despite the golf premium. Mr. Ian Cording, General Manager at The Bluffs Grand Ho Tram Strip, identifies the longer-term challenge:

“In parallel with developing tournament movements, Vietnam needs to further strengthen training in golf industry management domestically in Operations, Training, Sales & Marketing, to be able to deliver services at an international standard quality. Typically, in the South, the number of golf rounds on weekdays is lower compared to weekends.”

Cording’s observation cuts to the heart of Vietnam’s long-term competitiveness issue. Today, Vietnam wins on novelty, coastal beauty, and courses like The Bluffs that justify premiums. But as Cambodia upgrades facilities, Thailand maintains service standards, and Indonesia develops Bali alternatives, Vietnam’s tax burden becomes harder to justify.

What Is Being Done?

On March 7, 2026, Vietnam’s golf industry gathered for an unprecedented forum: “Removing Bottlenecks – Elevating Vietnamese Golf.” The proposed Vietnam Golf Investment Alliance (VGIA) aims to unify operators, developers, and stakeholders to advocate for related issues. Read more

The case is compelling: golf revenue is expected to contribute $1 billion annually to tourism (as part of a $10 billion sports economy target by 2040), yet faces a tax structure designed to discourage harmful luxury consumption. The proposed solutions are: First, policy reform must reframe golf as an economic and tourism industry, while correcting the tax structures that currently work against it. Second, a clearer and more flexible legal framework is needed to shorten project development timelines and unlock investment. Third, stronger cross-sector coordination is essential to build a nationally unified “Vietnam Golf” brand capable of competing on the international stage. Finally, the industry must develop a Green Golf model aligned with ESG standards and digital transformation, embedding sustainability at the core of the sector’s long-term growth.

Cording is cautiously optimistic:

“Some golf courses just opened, and it looks like many more are building now, which is great for the country. This demonstrates confidence despite the tax environment.”

But confidence and momentum do not guarantee policy change. Reform, if it comes, will be gradual.

Cambodia’s golf sector carries a 21% combined tax burden in 2026, among the highest in the region outside Vietnam. But as detailed in our recent article on Cambodia’s Tourism Struggles, taxation is far from the sector’s primary problem.

Jake Dudley, Golf Operations Manager at Phokeethra Country Club, shares the ground-level reality:

“It has been a very big challenge with the loss of direct flights from Korea. There have been no direct flights since 2024. The local market is gradually increasing, but Siem Reap golf still relies heavily on the international market.”

When asked about recent tax changes, Dudley’s response is revealing:

“No recent changes in golf-related taxation or policies.”

This illustrates Cambodia’s broader challenge. Tax policy matters little when:

• Flight connectivity doesn’t exist. Korean golfers, historically Cambodia’s largest segment, can no longer get there directly.

• Reputation crises persist, online scam coverage has devastated Cambodia’s image globally.

• Regional tensions continue, Cambodia–Thailand border conflicts closed key crossings, eliminating Thai weekend golfers.

Cambodia’s golf tourism declined an estimated 16.9% in 2025 despite hosting world-class courses like Vattanac and Phokeethra (a Faldo design). The problem is not course quality or taxation, it is infrastructure, connectivity, and perception.

Dudley’s closing observation captures the core issue:

“The last 2 years has highlighted how much we relied on the Korean market and the importance of targeting a wider market.”

Indonesia presents a fundamentally different model: moderate taxation combined with robust domestic demand creating stability that is far less dependent on volatile international tourism flows.

Mr. Shan Ramdas, General Manager at Handara Golf & Resort Bali, describes market conditions:

“We’ve seen a solid increase in total guest numbers compared to last year. What’s really been driving revenue is member referrals, they bring in high-quality guests and strong repeat potential. Interestingly, we’re also seeing more privately organized corporate events rather than those led by banks or government institutions.”

This shift toward private corporate events and member-driven business reflects Indonesia’s maturing golf culture, extending well beyond the traditional government and banking sectors. The domestic market provides a buffer that Cambodia, historically reliant on Korean tourists, has sorely lacked.

On Indonesia’s VAT, currently at 11%, Ramdas notes:

“Since tax is a fixed cost, any increase directly impacts operations, from service delivery to pro shop pricing and maintenance. When you combine that with the annual minimum wage increase, overall expenses can go up by around 5–10%. So naturally, operators need to adjust pricing strategies to keep everything sustainable.”

Indonesia’s 11% tax burden is absorbed through operational efficiency and pricing adjustments without materially damaging competitiveness. The combination of a moderate tax rate, Bali’s enduring global appeal, and a growing domestic market creates sustainable growth that isn’t hostage to any single policy or source market.

The Philippines operates with 12% VAT, positioning it squarely in the moderate range. What distinguishes the Philippines isn’t tax policy, however, it’s demographics.

Mr. Nimrod Quiñones, General Manager at Alta Vista Golf and Country Club, Cebu, shares:

“There is a rapid increase in local golfers, mostly young people.”

This youth participation surge is the inverse of the aging demographics seen in Japan, Korea, and Western markets. While Vietnam pushes for tax reform and Cambodia rebuilds its tourism ecosystem, the Philippines quietly builds a domestic golf culture among younger players creating long-term demand resilience that no tax policy change can replicate.

Mr. David Wong, Founder of Deemples, provides a characteristically concise update:

Malaysia: “8% Sales and Service Tax.”

Malaysia promotes golf as a sport by maintaining a competitive tax rate of 8% on golf services. Additionally, a 6% tax applies to food and beverage (F&B), and a 10% service charge — which directly benefits staff — is standard across the industry. This supportive tax environment encourages both participation and growth in the sport, with around 252 golf courses available across the country.

Malaysia recorded a remarkable 42.19 million international visitors in 2025, driven in part by record international air connectivity — over 168,900 international flights with more than 34.2 million seats offered. Chinese visitors reached 4.66 million, becoming the second-largest international visitor group. Malaysia’s SST has been stable since it replaced GST in 2018, and operators are not calling for change.

The competitive advantage of both markets lies not in any particular rate, but in predictability. Investors and operators know exactly what they are paying — enabling long-term planning that volatile policy environments consistently undermine. Compare this to Vietnam, where operators hope for reform but cannot plan around it, or Cambodia, where the market’s problems have little to do with taxation at all.

“GST for Singapore is currently at 9%.”

Singapore’s tourism sector achieved record results in 2025, welcoming 16.9 million international visitors and generating an unprecedented S$32.8 billion in tourism receipts. Golf tax remains stable at 9%, but Singapore’s golf landscape is being reshaped by a deliberate government policy to reclaim golf course land for housing and community use. Of the 16 remaining courses, several face lease expirations before 2035 without renewal. Warren Golf & Country Club, Orchid Country Club, Tanah Merah Country Club (Garden), Keppel Club (Sime), Singapore Island Country Club (Bukit), and Mandai Executive Golf Course are all affected. Sentosa Golf Club (Serapong) and the National Service Resort & Country Club (Kranji) have each been offered renewals until December 2040. For operators and members, the message is clear: plan around a contracting supply. Full details via the Ministry of Law Singapore.

Laos golf courses operate under a 28% Excise Tax on golf services, one of the higher rates in the region on paper, though its practical impact is limited by the market’s small scale. Courses serve primarily Thai cross-border golfers and expatriates, and the market is not yet large enough for tax policy to materially affect regional competitiveness.

Two developments signal gradual expansion: Savan Golf Resort in Savannakhet (a 9-hole Nicklaus Design layout, opened September 2025) and Thatluang Golf Village in Vientiane (an 18-hole Faldo Design course, expected Q3 2026 as part of the Thatluang Lake Park Special Economic Zone). Both are meaningful additions, but Laos remains a destination where course novelty and cross-border convenience matter more than tax arithmetic.

Mr. Simon Mees put it best: “Success will depend on differentiation through service quality, course conditioning, brand positioning, and total destination experience.”

He is right and those with a reasonable tax baseline to work from will be best positioned to deliver on it. Southeast Asia’s golf tax landscape in 2026 is not converging. It is diverging. Market leaders like Thailand extend their advantages through smart, deliberate policy. Emerging markets like Indonesia position competitively through moderation and domestic depth. And one outlier, Vietnam, is navigating its way upward through sheer market momentum, infrastructure investment, and an increasingly organized push for structural reform.

The market is evolving rapidly. We will report back as policy landscapes shift.

Acknowledgments

This report draws on survey responses and expert commentary from industry professionals working across Southeast Asia’s golf sector. We are grateful to:

Mr. Simon Mees – General Manager, Absolute Golf Solution Thailand

Mr. Ian Cording – General Manager, The Bluffs Grand Ho Tram Strip, Vietnam

Ms. Hien Ton – Director of Sales, Laguna Golf Lang Co, Vietnam

Mr. David Wong – Founder, Deemples (Malaysia / Singapore)

Mr. Jake Dudley – Golf Operations Manager, Phokeethra Country Club, Cambodia

Mr. Shan Ramdas – General Manager, Handara Golf & Resort Bali, Indonesia

Mr. Nimrod Quiñones – General Manager, Alta Vista Golf and Country Club, Philippines

And insights from several other leaders across the industry.

Additional information sources: PwC Worldwide Tax Summaries; Inland Revenue Authority of Singapore; PAJAK Indonesia; Avalara; Vietnam National Assembly Online; Garden City Golf Phnom Penh; Laos Country Club Golf Course; Vietnam Golf & Leisure Magazine; Ministry of Law Singapore. And to the Asia Golf Journey team for their dedication and contribution throughout this project.

Asia Golf Journey

Marketing Partner for Golf Courses and Resort Hotels in Southeast Asia

📧 creative@asiagolfjourney.com 📞 +84 982 117 466 🌐 www.asiagolfjourney.com

Data Collection Note: The data, expert insights, and market information presented in this report were collected by Asia Golf Journey between March and April 2026. Any developments, policy changes, tax amendments, or market shifts occurring after this period are not covered in this report and may not be reflected in the figures or analysis herein.

Disclaimer: Asia Golf Journey (AGJ) disclaims any liability for completeness, errors, or omissions contained herein and makes no representations regarding the accuracy, comprehensiveness, or suitability of the information provided. This collection has been curated by Asia Golf Journey, with contributions from various credited sources. AGJ undertakes no obligation to update, amend, or modify this report, or to notify readers in the event that any subject matter, opinion, forecast, or estimate contained in the report changes or becomes inaccurate